On Jan. 7, 2019, the U.S. Patent and Trademark Office (USPTO) published the 2019 revised patent subject matter eligibility guidance, regarding Section 101 and the test for “directed to an abstract idea.“ The guidance applies to all applications, and patents for applications, filed before, on or after Jan. 7, 2019. The guidance simplifies and makes more predictable the case law concepts of “an abstract idea” and of a claim “directed to” an abstract idea.

The guidance supersedes all conflicting sections of prior items in the Manual of Patent Examining Procedure, prior guidance and prior memoranda. The guidance states that “all USPTO personnel, as a matter of internal agency management, are expected to follow the guidance.” The guidance also states that “any claim considered patent eligible under prior guidance should be considered patent eligible under this guidance.”

We can expect that contemplated guidance will increase the allowance rates in art units handling software and business method cases (which rates currently are in single digits in some cases), to be much closer to the patent office allowance rates in art units not affected by the Alice Corp. v. CLS Bank International decision.

The 2019 revised guidance closely follows remarks by the director of the USPTO, Andrei Iancu, regarding the then-contemplated guidance, at the Intellectual Property Owners Association 46th annual meeting on Sept. 24, 2018.

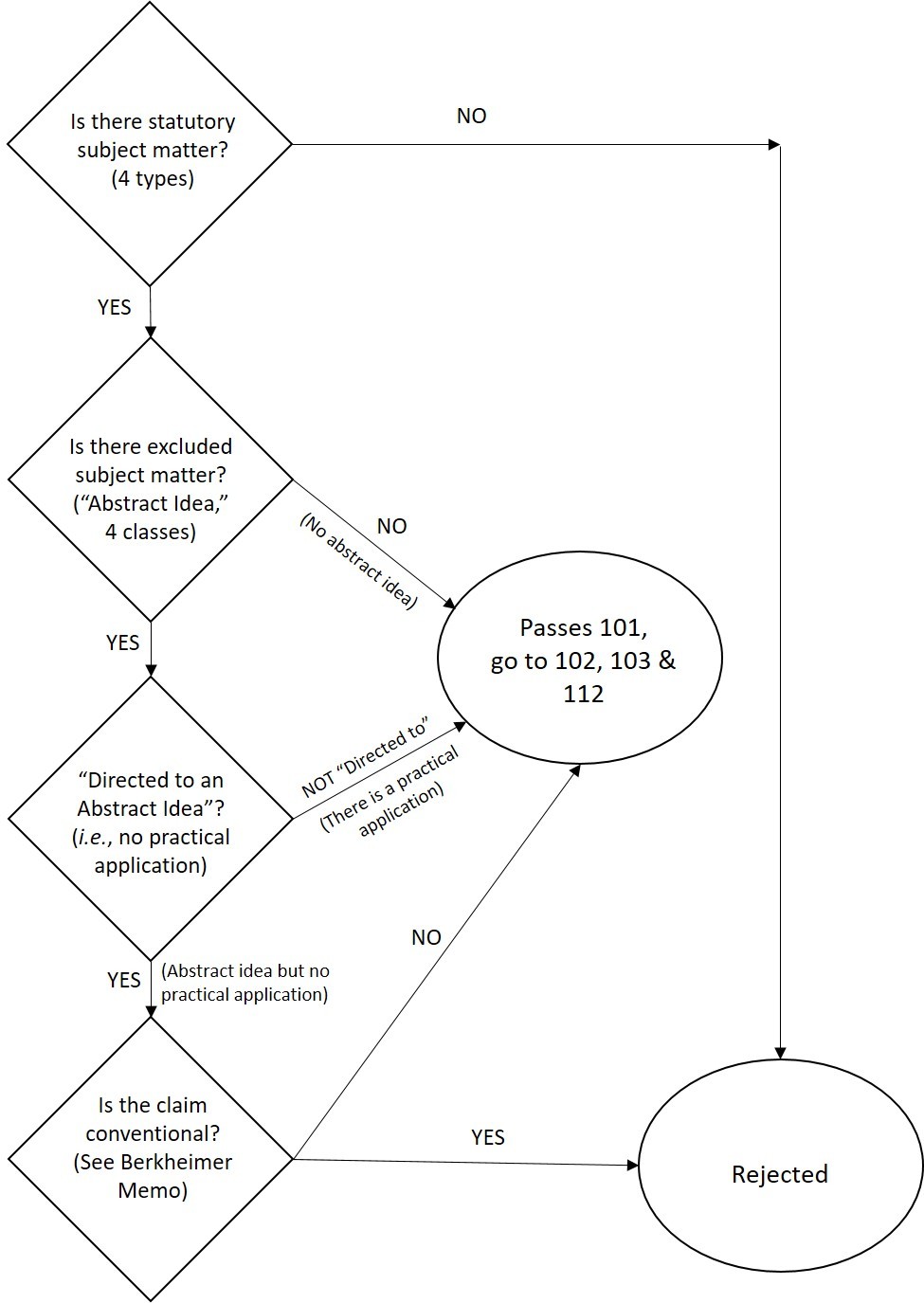

The 2019 revised guidance can be summarized and restated as a simplified process of four questions to apply the Alice-Mayo test for a Section 101 analysis. The four questions are graphically summarized in the flowchart included below, which we prepared for the convenience of the reader. The reader is invited to review the entire text of the guidance and the director's remarks at the IPO meeting for a complete description of the process.

The first of the four sequential questions: Is there statutory subject matter? There are four types of statutory subject matter: process, machine, manufacture, and composition of matter. If the answer to this question is no, then the claim is rejected. If the answer to this question is yes, then the examination goes to the second question.

The second question: Is there excluded subject matter? The subject matter excluded by case law from the Section 101 statutory classes is also referred to as abstract ideas. There are four types of excluded subject matter, or abstract ideas, which are discussed in more detail below. They include natural phenomena, mathematical concepts, certain methods of organizing human interaction, and mental processes performed in the human mind. If the answer to this question is no, there are no abstract ideas in the claim, then the claim passes the 101 Alice test, and the prosecution moves on to 102, 103 and 112. If the answer is yes, there is an abstract idea in the claim, then the prosecution goes to the third question.

The third question: Is the claim "directed to" the abstract idea? The claim is "directed to" the abstract idea if the claim fails to integrate the abstract idea into a practical application, and leaves the abstract idea as an unapplied general principle. If the claim has a practical application of the abstract idea, then the claim is not directed to the abstract idea. If the answer to this question is no, the claim is not directed to the abstract idea and does have a practical application, then the claim passes the 101 Alice test, and the examination goes to 102, 103 and 112. If the answer to the question yes, there is an abstract idea but no practical application, then the prosecution moves to the fourth question.

The 2019 revised guidance includes a nonexhaustive list of five examples of abstract ideas that have been successfully integrated into a practical application: (1) The claim reflects an improvement in the functioning of a computer, or other technology, (2) the claim applies the abstract idea to a particular treatment or prevention of a medical condition, (3) the abstract idea is used in conjunction with a particular machine or manufacture that is integral to the claim, (4) the abstract idea effects a transformation of a particular article to a different state or thing, and (5) the claim applies the abstract idea to a technology such that the claim does not monopolize the abstract idea.

The fourth question: Is the claim conventional? The procedure to answer this question is contained in the PTO guidance of 2018 found in the Berkheimer memo. If the answer to this question is no, the claim is unconventional, then the claim passes the 101 Alice test, and the examination goes on to 102, 103 and 112. If the answer to this question is yes, the claim is conventional pursuant to the Berkheimer memo, then the claim is rejected.

The 2019 revised guidance, and the director's prior comments to the IPO, make several other interesting points that can be summarized in five statements.

First, Section 101 analysis is distinct and should not include any elements of Section 102, 103 or 112 analysis. The case law for 102, 103 and 112 is old and well-developed, and not altered by Alice or Mayo.

Second, the subject matter excluded from the Section 101 explicitly eligible subject matter, i.e. the “abstract ideas” which are the focus of the guidance, are limited to four classes: (1) pure discoveries of nature (natural phenomena) or laws of nature, such as gravity, electromagnetism, DNA, etc., all of which are natural and before human intervention or application, (2) mathematical concepts like mathematical relationships, formulas, and calculations, such as calculus, (3) certain methods of organizing human interactions, such as fundamental economic practices (e. g., market hedging and escrow transactions); commercial and legal interactions; managing relationships or interactions between people; and advertising, marketing and sales activities, and (4) mental processes, which are concepts performed in the human mind, such as forming an observation, evaluation, judgment or opinion.

Regarding the question of whether a claim contains an abstract idea, the 2019 revised guidance states “in the rare circumstance in which an examiner believes a claim limitation that does not fall within the enumerated groupings of abstract ideas should nonetheless be treated as reciting abstract idea ('tentative abstract idea'), the examiner should evaluate whether the claim as a whole integrates the tentative abstract idea into a practical solution.” This is to be done in the same manner described herein for an abstract idea, regarding the third question: Is the claim “directed to” the abstract idea? If the examiner then finds that the tentative abstract idea is not integrated into a practical application and should be rejected, the examiner must bring the application to the attention of the technology center director. Any rejection that does not fall within the enumerated abstract ideas, that is nonetheless treated as an abstract idea, must be approved by the technology center director, and so noted in the file with a justification for treatment as reciting abstract idea.

Third, even if a claim contains an abstract idea, the claim is patent-eligible under 101 if the claim integrates the abstract idea into a practical application, and the abstract idea is not left as a mere principle without practical application in the claim. In that case, the prosecution moves to 102, 103 and 112 analysis, and the issue in the Berkheimer memo regarding “conventionality” is not reached and is not relevant.

Fourth, applying the test for "directed to," i.e., whether a claim with an abstract idea integrates the abstract idea into a practical application, thereby satisfying the 101 test, would dispose of the vast majority of cases.

Fifth, the guidance will ensure increased clarity in the patent system, and thus ensure that the United States continues to lead the world in innovation and technological development.

Basically, the 2019 revised guidance represents a swing of the pendulum in the pro-patent direction, that will counteract the preceding anti-patent swing culminating in the Alice case in 2014. This continues a pro-patent trend that the PTO began in the spring of 2018 with the issuance of the Berkheimer memo. Indeed, early statistics indicate that since the Berkheimer memo was issued, allowance rates at some art units, particularly for software, have gone up. We can expect this pro-patent trend to continue, partly because of a shift in the national discussion about patent law, from a focus on patent trolls to a focus on the protection of U.S. innovation in a competitive global economy.