This alert is the result of a collaboration between Akerman lawyers and real estate professionals at JLL.

Los Angeles property owners face a new transfer tax with the recent passage of the United to House LA measure (Measure ULA). With the intentional misnomer “Mansion Tax,” owners of any and all real property assets valued at over $5 million will now have a hefty portion of the sale put towards an initiative to address homelessness and other housing issues in LA. We explain the structure of the new measure, including tax exemptions and what the funds will be used for, discuss the pushback seen so far, and take a look at other similar measures that have been enacted elsewhere in California.

Overview

Measure ULA, initially put on the November 8, 2022 ballot by a coalition of housing advocates and labor unions, passed with approximately 57 percent support in the election[1]. Measure ULA establishes a new “Homelessness and Housing Solutions Tax” within the City of Los Angeles, imposed on the sale or transfer of real property valued at over $5 million, to fund affordable housing and tenant assistance programs.

Tax Structure

Under Measure ULA, starting on April 1, 2023, the new tax will be imposed on each and every deed, instrument, or writing by which any lands, tenements, or other realty sold within the City of Los Angeles are granted, assigned, transferred, or otherwise conveyed to, or vested in, the purchasers or any other persons when the consideration or value of the interest or property conveyed exceeds:

(1) $5,000,000 but less than $10,000,000, a tax at the rate of 4 percent of the consideration or value; or

(2) $10,000,000 or greater, a tax at the rate of 5.5 percent of the consideration or value.

The gross sale price of the property is the metric for the purposes of Measure ULA and will include the value of any lien or encumbrance remaining on the property at the time of sale. This is different from the existing documentary transfer tax imposed by the City and County of Los Angeles. For example, while the existing documentary transfer tax is calculated by excluding the value of any liens or encumbrances remaining on the property at the time of sale, the Measure ULA tax is imposed on the gross sale price of the property. The new tax would apply to the entirety of the sale consideration, not solely the amount in excess of the $5 million and $10 million thresholds, and regardless of whether the property is sold at a gain or a loss. The new tax is not calculated based on a tax progressive method, nor is it limited to one real estate asset class—every class from single family homes to office towers will be subject to the same tax regime.

The property value threshold subject to the tax would be adjusted annually based on the Chained Consumer Price Index.

The City of Los Angeles Finance Director is tasked with preparing regulations that will provide more details on calculations and enforcement. One of the first expected regulations will subject the transfer of ownership interests in an entity owning real estate to such tax. Also expected are exemptions that will track those in place for the documentary transfer tax, such as foreclosure and estate planning transfers.

Exemptions

Measure ULA also contains certain exemptions.

1. Qualified Affordable Housing Organization

The new tax shall not apply if the transferee is qualified as one of the following:

(1) a nonprofit entity within Internal Revenue Code Section 501(c)(3);

(2) a community land trust;

(3) a limited-equity housing cooperative; or

(4) a limited partnership or limited liability company in which only bona fide nonprofit corporations, community land trusts, and/or limited-equity housing cooperatives are the general partners or managing members.

To qualify for this exemption, the transferees must demonstrate a history of affordable housing development and/or affordable housing property management experience as determined by the Los Angeles Housing Department according to a procedure that will be promulgated by the Los Angeles Housing Department.

Community land trusts and limited-equity housing cooperatives may qualify for an exemption under this subsection without demonstrating a history of affordable housing development and/or affordable housing property management experience by (a) partnering with experienced nonprofit organizations such as the Los Angeles Housing Department or its successor agency; or (b) recording at the time of acquisition an affordability covenant.

2. Other Exemptions

The new tax is not applicable if a transferee is qualified as one of the following:

(a) a nonprofit entity within Internal Revenue Code Section 501(c)(3) which received its initial Internal Revenue Service determination letter at least ten years prior to the purchase and has assets of less than $1 billion;

(b) the United States or any agency or instrumentality, any state or territory, or political subdivision thereof, or any other federal, state, or local public agency or public entity; or

(c) any other transferee exempt from the city’s taxation power under the state or federal Constitutions.

Also, the Los Angeles City Council reserves the right to enact ordinances to exempt the new tax for real property acquired by nonprofit organizations to produce income-restricted affordable housing.

Use of Mansion Tax Revenues

The Measure ULA initiative is expected to generate approximately $600 million to $1.1 billion annually for existing and new programs. The Treasury of the City of Los Angeles will create and establish a special trust fund to be known as the “House LA Fund” for the deposit and use of all taxes collected under Measure ULA. Money in the House L.A. Fund shall be used exclusively according to the Los Angeles Program to Prevent Homelessness and Fund Affordable Housing (House LA Program). Some of the goals of the House LA Program include subsidizing housing, preserving affordable homes, preventing homelessness, and guaranteeing counsel to tenants in eviction court. The House LA Citizens Oversight Committee will be established to ensure the House LA funds are implemented and used consistently with the goals of the House LA program.

Amendment

The Los Angeles City Council may amend any provisions of the Measure ULA initiative, provided, however, that (1) such amendments must further or facilitate the purposes for the House LA Fund, and (2) no such amendment may increase the tax imposed without the voter approval required by Article XIII of the California Constitution (Proposition 13), among others.

Reactions and Challenges

Since Measure ULA’s passage, wealthy homeowners have already begun strategizing on ways to avoid paying the new tax upon a sale of their properties. Some homeowners are looking into splitting up their properties into smaller parcels with different ownership entities to avoid the tax altogether. For example, if a homeowner is selling a mansion for $15 million, there would be an $825,000 tax bill. But if the homeowner split up the property into three parts owned by three different entities and sold all three pieces for $4.99 million each, they would hypothetically avoid the new tax, as the levy starts at $5 million. As of now, it is unclear if the consideration or property values will be determined on a per property basis or in the aggregate for portfolio sales that involve more than one parcel of real property in the City of Los Angeles.

Another strategy might be to restructure the deal to keep a property sale under $5 million, which can be illegal. For example, if a seller wanted $6 million for their house, they could reach a deal with a buyer to sell it for $4.9 million, thus avoiding the tax, but then sell the furniture in the home for $1.1 million.

On or about December 21, 2022, a coalition of real estate and antitax groups, the Howard Jarvis Taxpayers Association and the Apartment Association of Greater Los Angeles, filed a lawsuit in the Los Angeles County Superior Court seeking to prevent the City of Los Angeles from implementing Measure ULA (Howard Jarvis Taxpayers Association, et al. v. City of Los Angeles, et al., No. 22STCV39662, Complaint, filed on December 21, 2022). The plaintiffs seek to invalidate the tax on the grounds that neither the City of Los Angeles nor its voters have the power to impose a special transfer tax without violating the California Constitution (Proposition 13). While some transfer taxes have been permitted in California charter cities, the complaint states, “transfer taxes that are ‘special taxes,’ however, are prohibited for all local governments.” It further argues that Measure ULA is actually a special tax because the revenue it would generate is specifically dedicated to housing and homeless services. In the complaint, the plaintiffs argue that “great and irreparable harm will result to plaintiffs, and to all Los Angeles property owners in being required to pay unconstitutionally imposed taxes,” and that “similar harm will occur to all Los Angeles residents in the form of increased rent and consumer prices resulting from the tax increase on all property sold (or value transferred) above $5 million.”

Others have pushed for repeal of Measure ULA through the ballot box. According to the California Secretary of State, a new state ballot initiative, backed by Kilroy Realty, seeking to invalidate the law has collected more than one million signatures, enough to place it on the ballot for the 2024 election.

Lastly, it’s not clear yet if the City of Los Angeles will start administering the tax on April 1, 2023, as scheduled, given the pending litigation. In a similar situation in San Francisco in 2017, the proceeds from a tax seeking to remedy homelessness were collected but placed in an escrow account while that tax was being challenged.

Analysis re: Similar Measure in Other Parts of the State

Between 2010 and 2020, there were 20 ballot initiatives to raise transfer taxes in California, 13 of which were approved by voters.

San Francisco, for instance, currently has a six-tier system that starts at 0.5 percent for sales above $100 and maxes out at 6 percent for sales above $25 million. The most recent new transfer tax in San Francisco, known as Proposition I, which was approved in November 2020 and became effective on January 1, 2021, raises the transfer tax rate on properties in the City of San Francisco that sell for more than $10 million. For properties sold between $10 million and $25 million, the rate increased from 2.75 to 5.5 percent on January 1, 2021. For properties sold for more than $25 million, the rate increased from 3 to 6 percent on January 1, 2021. A recent analysis by the San Francisco Comptroller estimated that doubling the transfer tax on high value properties reduces investment in commercial properties by $193 million annually and reduces investment in residential properties by $300 million annually.

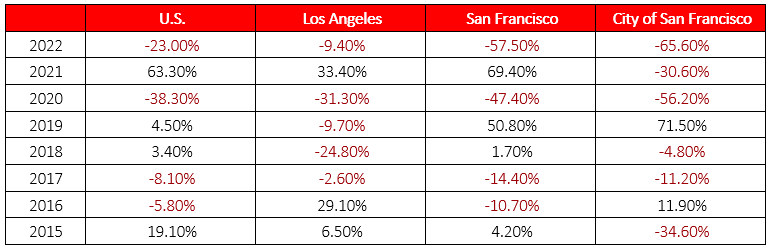

Exhibit 1 lists the annual growth in sales volume for the country as a whole compared to the two major cities in California, San Francisco, and Los Angeles. The chart shows the effects of higher transfer taxes in these two cities, each of which has experienced more years of negative volume growth than the rest of the nation. In short, transfer taxes have a major impact on sales volume and therefore on adaptive reuse and property investment levels.

Exhibit 1: 12-month Sales Volume Growth

Source: JLL Research and Real Capital Markets

Conclusion

As things stand, Measure ULA will go into effect on April 1, 2023, though the pending lawsuit brought by the Howard Jarvis Taxpayers Association and the Apartment Association of Greater Los Angeles may impact the immediate distribution of the funds collected. Should the measure pass muster in court, Los Angeles could expect to see a cooling effect on investment in real estate, following San Francisco's lead.

[1] Measure ULA only needed a simple majority to pass. Special taxes historically required a two-thirds majority, but in a 2016 ruling, a California state appeals court held that the higher bar for a special tax only applies to ballot measures sponsored by legislators and that ballot measure brought by citizens could pass by a simple majority vote. The California ballot initiative process gives California citizens a way to propose laws and constitutional amendments without the support of the Governor or the Legislature. Measure ULA has thus become law by 57 percent of the city’s voters in a referendum.