In an effort to encourage the creation of new housing in certain areas of our nation’s capital, the District of Columbia has launched a program offering tax abatements to commercial property owners who convert their properties (or portions of them) into residential housing.

The Housing in Downtown Tax Abatement program was signed into law in July 2022, and is codified at D.C. Code § § 47-860.01 - 47-860.04. Under the program, certain commercial property owners are eligible for an abatement of real property taxes for a period of 20 years, as long as certain conditions are met, including the following:

- There is a change in use resulting in the development of at least 10 housing units.

- At least 15 percent of the housing units are developed or redeveloped as affordable housing.

- The affordable housing units are designed and administered in accordance with the requirements of the Inclusionary Zoning Program.

- The owner must contract with certified business enterprises for at least 35 percent of the construction and operations costs of the project.

- The owner must execute a first source agreement for the construction and operation of the project.

- The mayor provides a letter stating that the proposed project is eligible for the tax abatement and setting forth the expected amount of the abatement.

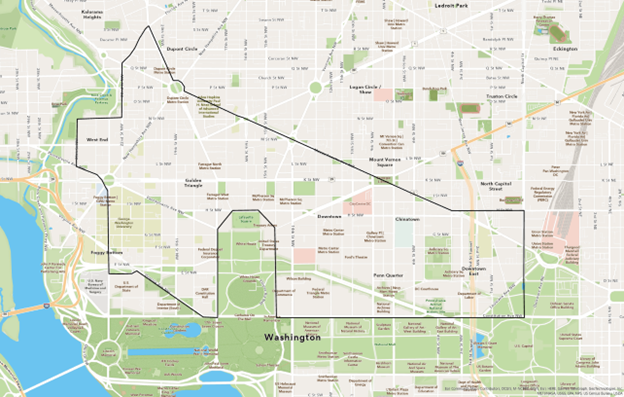

- The property is within the following “eligible area”:

The tax abatement amount is determined by the mayor and is based on residential floor area ratio (FAR) square foot of real property, multiplied by the building’s total residential FAR square footage. The mayor’s office has indicated that “there is no set percentage for abatement, and the amount will be awarded on a case-by-case basis.”

The tax abatement is capped in FY24, FY25, and FY26 at $2.5 million, but that number rises to $6.8 million in FY27. Every year after, the abatement cap rises by 4 percent from the prior year (i.e., 104 percent of the prior year’s limit).

The tax benefits begin in the tax year in which a certificate of occupancy is issued, and expire at the end of the 20th tax year thereafter.

The deputy mayor for Planning and Economic Development (DMPED) is responsible for issuing regulations for and administering the program. DMPED anticipates issuing regulations and a request for applications following the finalization of the FY24 budget, which is expected to occur in July 2023. We anticipate that such regulations may include a mechanism for determining the amount of abatement offered.

The foregoing is not intended to constitute legal advice, and only provides a summary of certain elements of the Housing in Downtown Tax Abatement program. Akerman attorneys can assist with understanding the program’s full requirements and with navigating the application process.